Ah, mortgages—the love-hate relationship we all aspire to have someday. They help you buy your dream home, but they also come with a few extra costs that can feel like they’re there just to keep things interesting. Today, we’re tackling one of those pesky extras: **private mortgage insurance**, or PMI. Spoiler alert—it’s not the kind of insurance you’ll want to brag about.

So, What Exactly is PMI?

Picture this: You’ve found your dream home in Portland Metro. You’re crunching numbers, working out your down payment, and bam—you realize you’re not quite at 20% of the purchase price. That’s when PMI enters the chat.

PMI is like the safety net your lender insists on having in case you stop making payments. If your down payment is less than 20%, your lender sees you as a slightly riskier bet. PMI protects *them*—not you—if you default on the loan and the home ends up in foreclosure.

How Much Does PMI Cost?

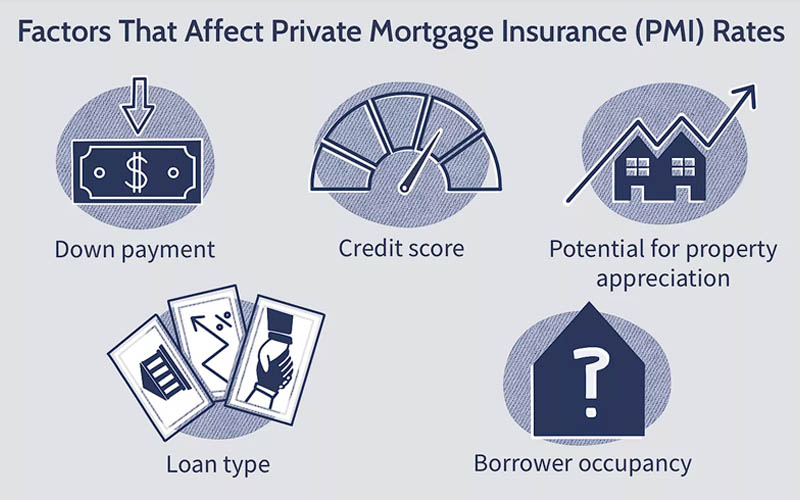

Here’s the kicker: PMI typically costs between **0.3% and 1.2% of your loan amount per year. That might not sound like much, but on a $400,000 home, that’s $1,200 to $4,800 a year. Ouch.

Your exact PMI rate depends on a few factors:

- Your credit score (good credit = lower rate)

- Your down payment size (the smaller the down payment, the higher the PMI)

- Your loan terms

And how do you pay for it? Usually, it’s baked into your monthly mortgage payment alongside property taxes and interest. But if you’re feeling bold—or flush with cash—you might be able to pay the full PMI upfront at closing.

When Can You Say Goodbye to PMI?

Here’s the good news: PMI isn’t forever (unless you let it be).

PMI is the unwelcome houseguest that sticks arounds until you’ve built 20% equity in your home, you can ask your lender to cancel your PMI. Better yet, once you hit 22% equity, your lender is legally required to remove it for you. (Finally, some relief!)

Pro Tip: Keep an eye on Portland Metro’s property values. If your home appreciates faster than expected, you could reach that 20% equity threshold sooner than you thought. Another option? Refinancing your mortgage, which could eliminate PMI and potentially score you a lower interest rate while you’re at it.

How to Get Rid of PMI in Portland Metro and Clackamas County

- Pay Extra on Your Mortgage Each Month

One straightforward (but not always easy) way to get rid of PMI is to pay extra on your mortgage every month. By chipping away at your principal faster, you’ll build equity sooner and reach that coveted 80/20 loan-to-value (LTV) ratio.

Let’s break it down:

Imagine your Portland home was purchased for $500,000, and you put down 10%. That leaves you with a $450,000 mortgage. To reach 20% equity, you’ll need to pay down your balance to $400,000. Paying even $200–$500 extra a month can shave years off your PMI timeline.

But let’s be real—finding extra cash every month isn’t always doable. If you’re just starting out and saving for a home, consider this: waiting an extra year or two to save up for a 20% down payment might help you avoid PMI altogether.

- Get a New Home Appraisal

Here’s a trick that works especially well in the Portland Metro area and Clackamas County, where home values tend to climb over time. If property values in your neighborhood are on the rise, your home equity might be growing faster than you think.

Equity is the part of your home you actually own—your down payment, plus the value of any appreciation, minus what you still owe on your mortgage. For instance, if your Clackamas County home has appreciated significantly in the past few years (not uncommon with Portland’s steady demand), your equity could be higher than you realize.

If you suspect your home’s value has increased enough to tip your equity past the 20% mark, consider paying for a new appraisal. You’ll have to front the cost (usually a few hundred dollars), but if the appraisal confirms you owe less than 80% of your home’s new value, you can ask your lender to cancel PMI.

- Keep an Eye on Refinancing Opportunities

Mortgage rates fluctuate, and a rate drop could be your golden ticket to refinancing. A refi not only helps you potentially lower your interest rate, but it can also help you hit that 80/20 LTV ratio if your home’s value has increased.

Here in Oregon, where the market often benefits from an influx of new buyers and increasing property values, refinancing can be a smart move. Just make sure the savings outweigh the costs—talk to a trusted lender to run the numbers. I have several mortgage advisors and lenders that I would be happy to introduce you to. Five star professionals that have been in the lending business over 30+ years.

PMI: The Necessary Evil

They say PMI stands for “Private Mortgage Insurance,” but let’s be honest—it feels more like “Pay More Immediately.” Or maybe “Please Make it Invisible!” (We’re working on it.)

All jokes aside, PMI can be a financial drag, but it doesn’t have to stick around forever. With the right strategies and a little persistence, you’ll be waving it goodbye before you know it.

Need Help Navigating Your Options?

Whether you’re a first-time buyer or an experienced homeowner, the mortgage process can feel overwhelming. That’s why working with the right professionals is crucial. I can connect you with trusted lenders who know the ins and outs of PMI in Portland, Clackamas County, and across Oregon. Together, we’ll make sure you’re taking the smartest steps for your financial future.

Need More Info? Let’s Chat

Whether you’re shopping for a condo in the Pearl District, a single-family home in Lake Oswego, or a ranch in the Willamette Valley, I’m here to help. Not only can I walk you through the real estate process, but I can also connect you with trusted lenders who can explain your mortgage insurance options in detail—and maybe even help you avoid PMI altogether.

Let’s talk about how you can achieve your homeownership goals—and get rid of PMI faster. Contact me today, and let’s make it happen!

Suzanne Scott, Realtor GRI, ABR, PSA, SRES

suzanne(at)ScottRealEstateCollective(dotted)com 971.295.6087